Trade Data Supply Chain Demystified Part 1: Where Are My ICE Trades?

New Definitive Guide & Checklist for ICE Trades | Part One of Five This is the first in a series of five blogs examining the

Trade Data Supply Chain Demystified Part 2: ICE Trade Capture Unpacked

Tracking Trade Data from an Order to Instant Risk/PnL | Part Two of Five In this second post in our series of blogs discussing the

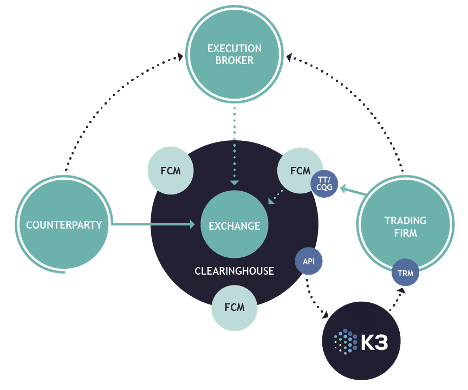

Trade Data Supply Chain Demystified Part 3: Real-Time Trade Data from the CME

General Data Flow for Futures Exchanges This is Part Three of our five-part series on demystifying the trade data supply chain. Be sure to read